Capital Gains Tax & Dividend Tax on PSX Stocks (Pakistan)

If you invest on the Pakistan Stock Exchange, two taxes touch almost everything you do: capital gains tax (CGT) when you sell shares for a profit, and dividend tax when a company pays you a dividend. This guide explains how both work in plain English, why your filer status matters more than almost anything else, and who actually calculates and collects these taxes so you are not left guessing.

One thing up front, because it matters for a topic like this: tax rates in Pakistan are set in the annual federal budget each June and can change from one year to the next. The figures below reflect the framework into the 2026-27 tax year, including the Finance Act 2026 passed in June 2026 (which, for ordinary listed-share investors, left the headline rates unchanged - details below). Treat them as a map of how the system works, not as a guaranteed number for your exact situation, and confirm the current rate with the official sources linked at the end before you act.

Key takeaways

- Two separate taxes: CGT applies to your profit when you sell shares; dividend tax applies to dividends you receive. They sit in different parts of the law (CGT under Section 37A, dividends under Section 150) and are collected differently.

- Filer vs non-filer is the biggest lever. Being on FBR's Active Taxpayers List (ATL) roughly halves the tax you pay on dividends and gives you the lower CGT treatment. Non-filers are taxed much more heavily.

- Acquisition date and holding period matter for CGT. When you bought the shares determines which rule set applies; very old holdings can be exempt or tiered.

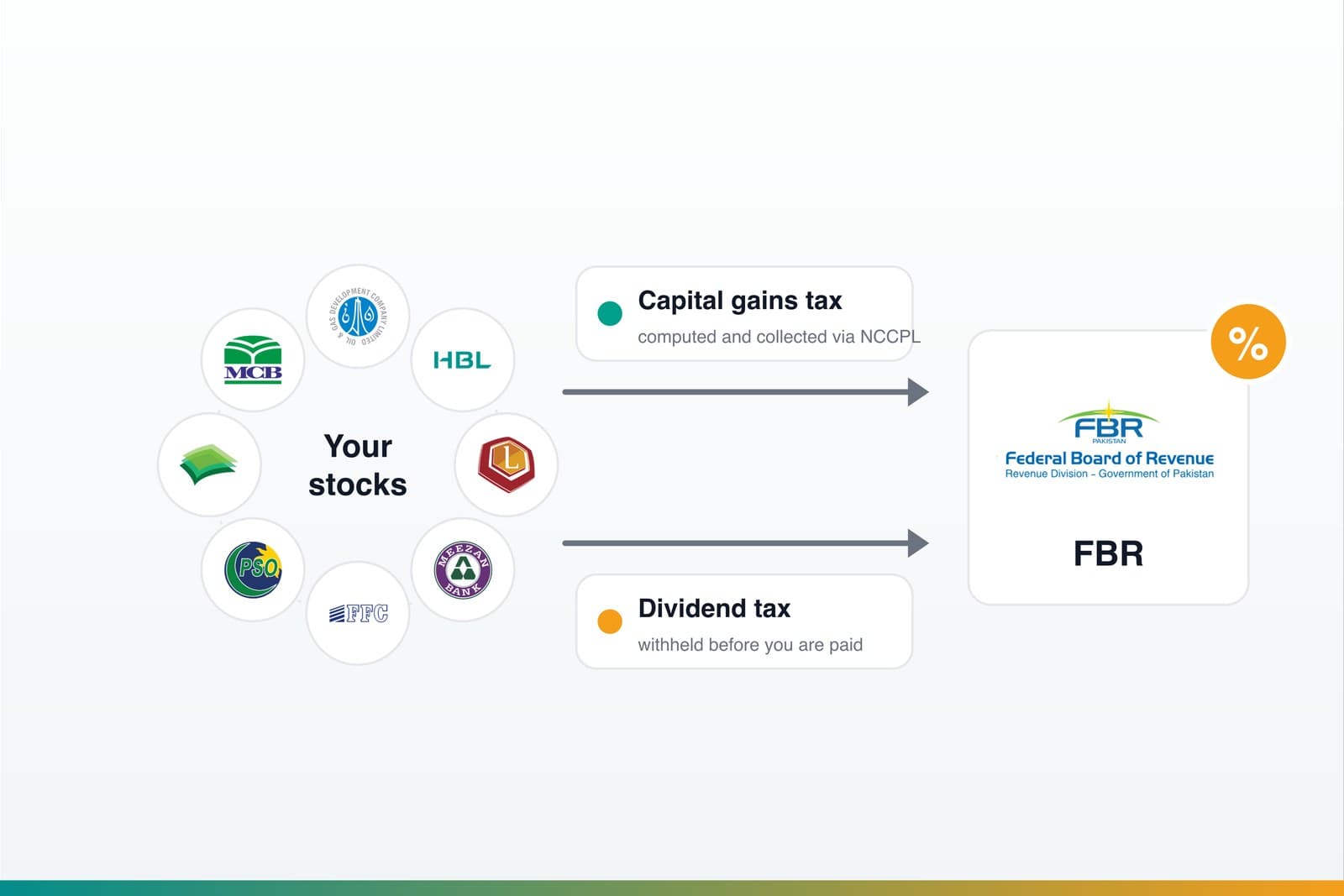

- You usually do not self-compute PSX CGT. NCCPL calculates it across your brokers and it is collected through settlement. Dividends are withheld at source. You still declare both in your annual return.

- Investify is a data and portfolio app, not a broker or tax adviser. It helps you see dividends and holding periods; the authoritative records are your broker/CDC account, the NCCPL statement and FBR.

The two taxes, side by side

| Capital gains tax (CGT) | Dividend tax | |

|---|---|---|

| When it applies | When you sell listed shares for a profit | When a company pays you a dividend |

| Law | Section 37A, Income Tax Ordinance | Section 150, Income Tax Ordinance |

| Who calculates/collects it | NCCPL, across your brokerage accounts | Withheld at source by the company/CDC before you receive it |

| How it is charged | Rate depends on acquisition date, holding period and filer status | Generally a flat rate on the gross dividend |

| Typical treatment | Collected via settlement; reconciled in your return | Usually a final tax on that income; still declared |

What the June 2026 budget changed (and what it didn't)

The Finance Act 2026 - the budget passed by the National Assembly in June 2026, effective from 1 July 2026 (tax year 2027) - is the first question every investor asks after budget season, so here is the short answer for the stock market:

- Listed-share CGT: unchanged. The 15% headline rate for people on the Active Taxpayers List continues to apply to shares acquired on or after 1 July 2024, and the heavier slab-based treatment for those not on the list continues for later acquisitions.

- Dividend tax on ordinary listed shares: unchanged. The ~15% filer / ~30% non-filer withholding picture carries into 2026-27.

- Debt securities: withholding increased. Tax withheld by custodians on gains from debt securities disposed of outside the exchange system rose from 15% to 20%. This touches investors holding bonds/Sukuk through IPS accounts, not ordinary PSX share trades.

- The high-income surcharge is abolished from tax year 2027. The surcharge previously levied under Section 4AB on high incomes goes away, which modestly lowers the all-in burden for high earners - separate from the CGT/dividend rates themselves.

- Context from the year before: the Finance Act 2025 changed how mutual fund dividends are taxed - split in proportion to the fund's income from equities (15%) versus debt (25%) - and that regime continues. If you hold funds rather than direct shares, this is the rule that shapes your dividend withholding.

In short: if you buy and sell listed shares and receive ordinary dividends, the 2026 budget did not move your rates. The changes live at the edges - debt instruments, funds and the surcharge.

Capital gains tax on PSX shares

CGT is a tax on the profit you make when you sell a share for more than you paid. If you sell at a loss, there is no gain to tax (and losses can generally be set against gains within the rules).

The important thing beginners miss is that the rate is not one single number - it depends on when you acquired the shares and, for some holdings, how long you held them, as well as your filer status. Broadly, the framework has worked like this:

| When you acquired the shares | How CGT has broadly applied |

|---|---|

| Before 1 July 2013 | Generally exempt from CGT. |

| 1 July 2013 - 30 June 2022 | A flat rate (historically 12.5%) regardless of holding period. |

| 1 July 2022 - 30 June 2024 | Tiered by holding period for filers - a higher rate for short holdings, tapering down to 0% for very long holdings - with heavier treatment for non-filers. |

| On or after 1 July 2024 | A 15% headline rate for people on the ATL (filers); substantially higher treatment for those not on the list. |

| On or after 1 July 2025 | 15% for ATL persons; those not on the ATL are taxed at normal slab / applicable rates, which can be higher than 15%. Confirmed unchanged by the Finance Act 2026 for tax year 2026-27. |

Who calculates PSX capital gains tax

For shares listed on the Pakistan Stock Exchange, you generally do not work out CGT trade by trade yourself. The National Clearing Company of Pakistan (NCCPL) computes capital gains tax across all your brokerage accounts, and it is collected through the settlement system. NCCPL provides a CGT statement you can access, which is the record you reconcile against.

What you should do is keep your own view of holdings, purchase dates and dividends, declare your capital gains in your annual income tax return, and check the NCCPL statement rather than assume it is complete - especially if you use more than one broker.

Dividend tax on PSX shares

When a listed company pays a dividend, tax is withheld at source - deducted before the cash reaches your account - under Section 150. For most listed companies the general position has been:

- Filers (on the ATL): around 15% on the gross dividend.

- Non-filers: roughly double, around 30%.

There are special cases where the rate differs. Dividends from certain independent power producers have carried a 7.5% rate, while dividends from companies that themselves pay no tax have been taxed at 25%. Mutual fund dividends follow their own regime since the Finance Act 2025: the withholding is split in proportion to the fund's income - the equity-derived portion at 15%, the debt-derived portion at 25%. For a normal retail investor holding ordinary listed shares, the 15% filer / 30% non-filer picture is the one to internalise - but if a specific holding looks different on your dividend advice, it is usually one of these special cases, and worth checking.

Filer vs non-filer: the lever you control

Almost everything above has a "filer" number and a "non-filer" number, and the gap is large. A filer is simply a person who appears on FBR's Active Taxpayers List (ATL) because they file their annual income tax return. A non-filer does not, and pays materially more on both dividends and capital gains.

For most retail PSX investors, becoming a filer is the single most effective tax move - it is not a loophole, it is just doing the basic compliance the system rewards. In practice that means registering with FBR, obtaining your NTN, and filing your annual return so that you land on the ATL. If you are unsure how to do this correctly, a tax practitioner can set it up once and it becomes routine thereafter.

Use Investify for your daily PSX workflow

Open market data, stock pages, charts, news, announcements, watchlists and portfolio tracking from one Investify account.

Open InvestifyA simple, hypothetical example

Numbers here are illustrative only, to show the shape of the calculation - not a rate quote for your situation.

Suppose a filer buys 1,000 shares at Rs 100 (Rs 100,000) and later sells them at Rs 130 (Rs 130,000).

- Capital gain: Rs 130,000 − Rs 100,000 = Rs 30,000.

- CGT at an assumed 15% filer rate: Rs 30,000 × 15% = Rs 4,500, computed and collected via NCCPL/settlement.

While holding, the company pays a Rs 5 per share dividend on 1,000 shares = Rs 5,000 gross.

- Dividend tax at an assumed 15% filer rate: Rs 5,000 × 15% = Rs 750, withheld before the Rs 4,250 net reaches the account.

A non-filer in the same scenario would pay noticeably more on both - which is the whole point of getting onto the ATL. Again: plug in the current, confirmed rates for your acquisition year rather than the assumptions used here.

What you still have to do yourself

Even though CGT is computed by NCCPL and dividend tax is withheld at source, you are not entirely hands-off:

- File your annual income tax return - this is what puts and keeps you on the ATL.

- Declare your capital gains and dividend income (and the tax already deducted) in that return.

- Reconcile the NCCPL CGT statement and your dividend advices against your own records, particularly if you trade through more than one broker.

- Keep records of purchase dates and costs, since acquisition date drives your CGT treatment.

How Investify helps (and where it stops)

Investify is a PSX market-data and portfolio-tracking app - not a broker and not a tax adviser or tax calculator. Where it helps at tax time is by giving you a clean, single view of the facts you need to hand to yourself or your adviser:

- Your holdings and how long you have held each position.

- The dividends your holdings have paid, and the announcements behind them.

- Your portfolio history as context for what you bought and when.

For the numbers that actually go on a return, rely on the authoritative records: your broker/CDC account, the NCCPL CGT statement, your dividend advices, and FBR's current rules. Any real tax decision should be checked against those sources, and with a qualified professional where your situation is not straightforward.

Educational and tax note

This article is general educational information about how PSX-related taxes work; it is not tax, legal, financial or investment advice, and it does not recommend buying or selling any security. Tax rates, thresholds and rules in Pakistan are set in the annual federal budget and can change each year, and specific situations vary. All rates mentioned are framework-level and illustrative, current to the 2026-27 tax year as set by the Finance Act 2026, and must be verified against the Federal Board of Revenue (FBR), NCCPL and, for company-law matters, SECP before you rely on them. For your personal position, consult a qualified tax professional. Investify is a PSX market-data and portfolio-tracking app and is not a broker or tax adviser.

The bottom line

Capital gains tax and dividend tax are less intimidating once you see the structure: CGT hits your profit on sale (rate driven by when you bought and your filer status, computed by NCCPL), while dividend tax is withheld at source on what companies pay you (~15% filer / ~30% non-filer in the ordinary case). The most powerful thing most investors can do is become a filer, declare everything in the annual return, and keep clean records - then confirm the exact current rates with FBR and NCCPL before acting.

Related reading

Sources and references

- Federal Board of Revenue (FBR)Income Tax Ordinance, current rates and the Active Taxpayers List (ATL).

- NCCPL - Capital Gains Tax (CGT)Computes and reports CGT for the capital market; source of your CGT statement.

- Securities and Exchange Commission of Pakistan (SECP)Company-law and capital-market regulation.

- PSX - Investor Resources and ToolsOfficial investor education for the Pakistan Stock Exchange.

- PwC - Pakistan Tax SummariesThird-party summary of dividend and capital-gains treatment.

- A.F. Ferguson / PwC - Tax Memorandum on Finance Bill 2026Professional commentary on the June 2026 budget's tax measures.

- KPMG - Budget Brief 2026 (Pakistan)Summary of Finance Act 2026 changes.